Search our website enhanced by Google.

See our stacking analysis on two other sectors:

Our analysis considers two ways of stacking actions:

Table 1 shows which actions were included in options A and B, along with payment rate and the area of the virtual farm selected for each action.

Note: The table shows current actions available.

Table 1. SFI and CS actions under Options A to C with payment rates and area of land

| Code | Action | Payment | Area or length | |

|---|---|---|---|---|

| Option A | CSAM1 | Assess soil, test soil organic matter (SOM) produce soil management plan | £6/ha plus £97 per agreement | 450 ha |

| CSAM2 | Multi-species winter cover crop | £129/ha | 75 ha | |

| CHRW1 | Assess and record hedgerow condition | £5 per 100m – one side | 23,200 m | |

| CHRW2 | Manage hedgerows | £13 per 100m – one side | 23,200 m | |

| CHRW3 | Maintain or establish hedgerow trees | £10 per 100m – both sides | 23,200 m | |

| CIPM1 | Assess integrated pest management and produce a plan | £1,129 per year | n/a | |

| CIPM3 | Companion crop on arable land | £55/ha | 31.5 ha | |

| CIPM4 | No use of insecticide on arable crops and permanent crops | £45/ha | 67.5 ha | |

| CNUM1 | Assess nutrient management and produce a plan | £652 per year | n/a | |

| PRF1 | Variable rate application of nutrients | £27/ha | 142 ha | |

| SOH1 | No-till farming | £73/ha | 76.5 ha | |

| SOH3 | Multi-species summer-sown cover crop | £163/ha | 140 ha | |

| Option B All actions listed for option A, plus: | CIPM2 | Flower-rich grass margins, blocks or in-field strips | £798/ha | 5 ha |

| CNUM3 | Legume fallow | £593/ha | 1.5 ha | |

| CAHL1 | Pollen and nectar flower mix | £739/ha | 5 ha | |

| CAHL2 | Winter bird food on arable and horticultural land | £853/ha | 5 ha | |

| CAHL3 | Grassy field corners and blocks | £590/ha | 4.5 ha | |

| CAHL4 | 4m to 12m grass buffer strip on arable and horticultural land | £515/ha | 0.4 ha | |

| AHW2 | Supplementary winter bird food | £732 per tonne | 2.5 t | |

| AHW9 | Unharvested cereal headland | £1,072/ha | 0.28 ha | |

| BFS4 | Protect in-field trees on arable land | £553/ha | 0.24 ha |

Source: Defra, AHDB

An SFI management payment is also available, which is £40/ha up to the first 50 hectares of land entered into the relevant SFI actions in the first the SFI agreement. In subsequent years, the management payment is £20/ha up to the first 50 hectares of land entered. This has been factored into the analysis: the virtual 455 ha arable farm receives the maximum SFI management payment of £2,000 in year 1 and £1,000 in years 2 and 3.

For this analysis, we used our 455 ha arable virtual farm. The AHDB virtual farms are theoretical farms that exist on a spreadsheet but are designed to be representative of ‘typical farms’. They have been created as middle 50%-performing businesses: this means that their performance is comparable to actual national or regional averages. The costs associated with these middle-performing farms also tend to be higher than on farms in the top 25%, and these costs have been cross-referenced to average results from the Farm Business Survey.

Detailed description of the arable virtual farm

The analysis used 2023 as the baseline year, as this is the most recent year for which there is a full set of annual data.

We allocated different areas of the farm to the individual actions under each option and calculated the cost of carrying out each of the SFI actions on that area. This provided a net payment for each SFI action.

Net payments were calculated for each of the three years of the SFI agreement, taking into account that one-off costs and annual costs were incurred, depending on the action.

To examine the effect on the farm of taking part in the SFI, all other variables – such as prices and yields – were kept constant over the three-year duration of the SFI agreement). The net payments were incorporated into the virtual farm’s balance sheets to calculate the net profit (total revenue minus total costs) for a given year. The change in the farm’s net profit in taking part in the SFI compared with not taking part in the SFI was then calculated.

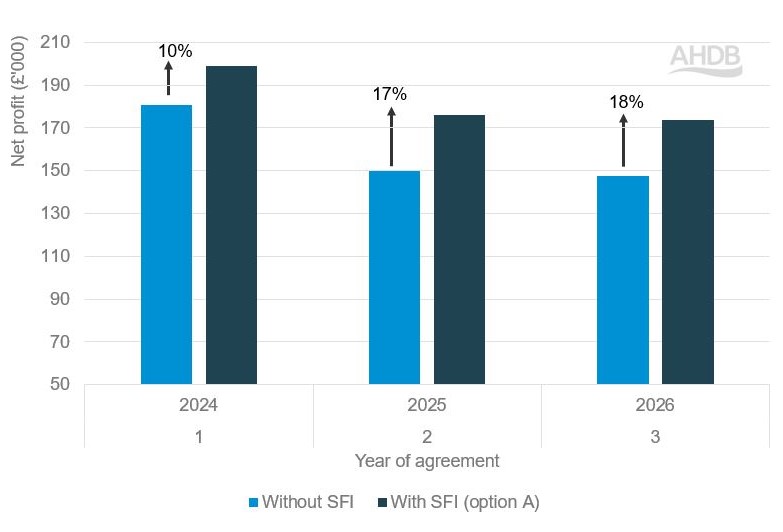

Figure 1 shows that the net profit (total revenue minus total cost) of the farm increases by 10–18% each year between 2024 and 2026.

Figure 1. Effect on 455 ha arable farm’s net profit level – option A

Source: AHDB

The gross profit of the 455 ha arable farm (using 2023 as a baseline) is £1,200/ha. If the gross profit was around £1,700/ha, the farm’s net profit would increase by 5% in year 1 and 8% in years 2 and 3.

The impact of the SFI is greater on farm businesses with low gross profit margins than those with high gross profit margins.

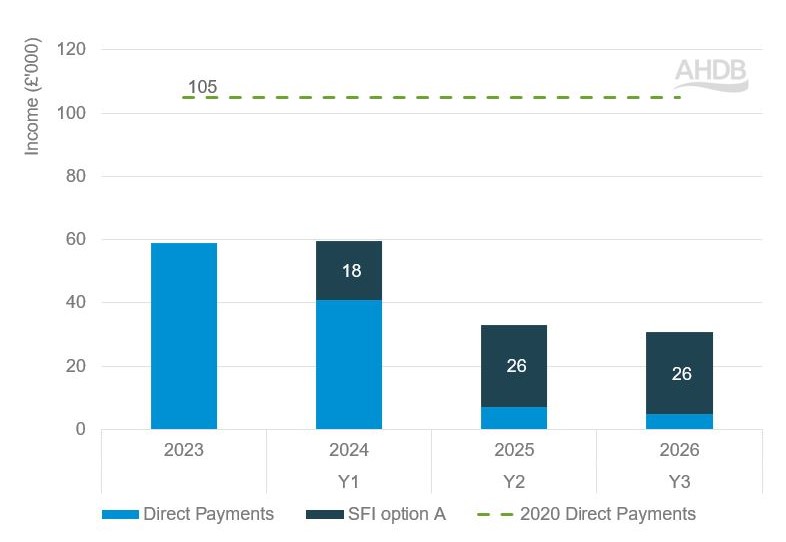

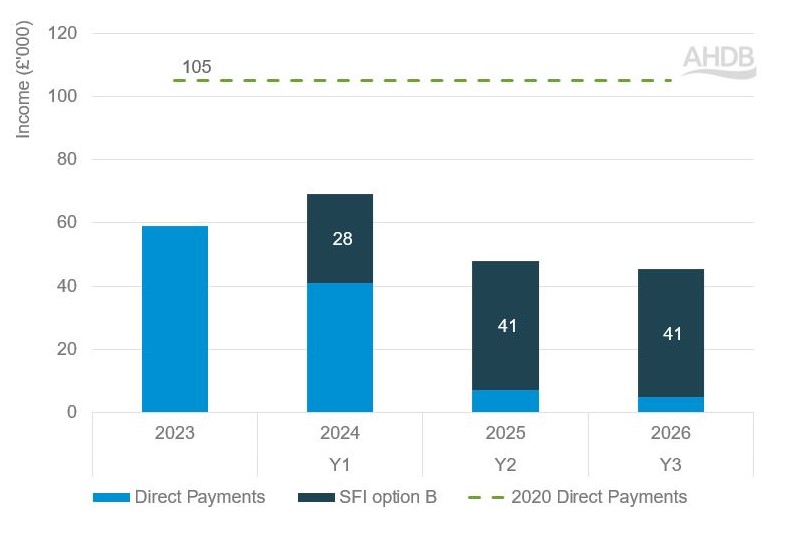

Figure 2 shows the income that would be received by AHDB’s 455 ha arable virtual farm if option A was selected.

Figure 2. Three-year projection of income received by a 455 ha arable farm from Direct Payments and SFI actions – option A

Source: AHDB

See a breakdown of SFI payments with option A

As a result of carrying out the actions under option A, the farm receives an extra £23,400 on average per year over the three-year duration of the SFI agreement.

While this does not fill the gap left by reduction of Direct Payments, it enables the farm business to be over £23,000 better off than it would have been without SFI.

Option A, therefore, provides the 455 ha arable farm with an average of £23,400 additional income per year and a 10–18% increase in net profit over the three years of the scheme and does not require any major changes to be made to the farm’s set-up.

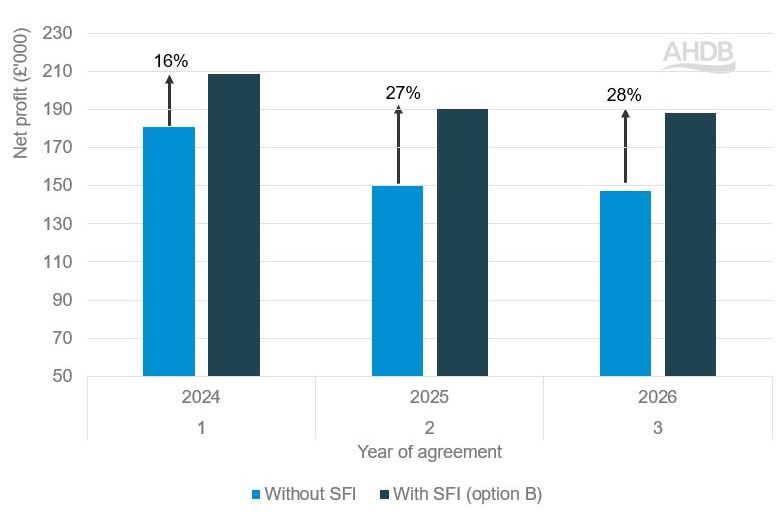

The more ambitious SFI actions require land and can potentially alter the set-up of the farm. To carry out the ambitious actions in option B, 22 ha of unproductive land was selected, which equates to 5% of the farmland available.

If the 455 ha arable farm has one or two unproductive fields, on which all of the ambitious SFI actions in option B can be allocated, the change in the farm’s net profit increases by 16–28% over the three years (Figure 3).

Figure 3. Effect on 455 ha arable farm’s net profit level after implementing option B on unproductive fields

Source: AHDB

The percentage changes shown in Figure 3 are based on a gross profit level of £1,200/ha. If the farm had a gross profit level of £1,700/ha, the percentage changes in years 1, 2 and 3 would be 3%, 12% and 12%, respectively.

Out of the ambitious actions within option B (Table 1), winter bird food on arable and horticultural land (CAHL2) offers the highest net payment on average for the 455 ha farm. At the time of writing, six SFI actions have area limits imposed on them whereby no more than 25% of the farm area can be entered into either a single or combination of these actions. Winter bird food on agricultural and horticultural land (CAHL2) is one such action.

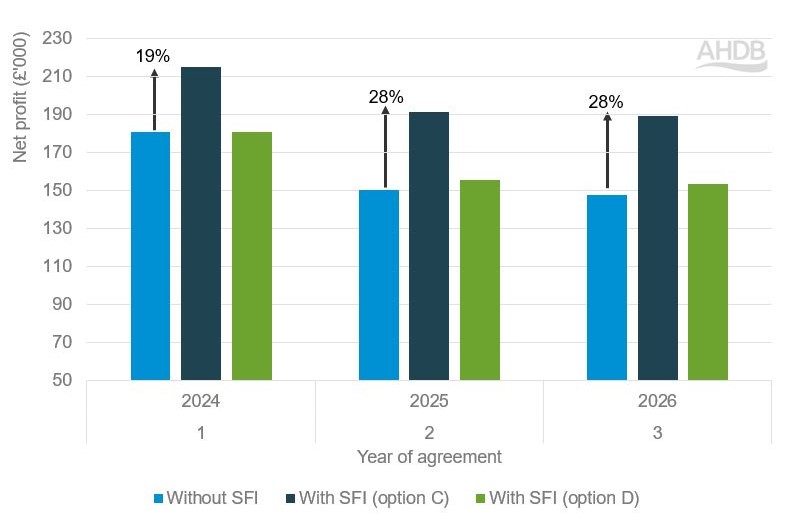

Two further options for the 455 ha farm were examined specifically for the winter bird food action:

If all 22 ha of unproductive land on the farm was entered into the winter bird food action (option C), the net profit of the farm increased by 19% in year 1, 28% in year 2 and 28% in year 3 as shown in Figure 4.

Figure 4. Effect on 455 ha arable farm’s net profit level after implementing option B by sacrificing productive land

Source: AHDB

A variety of SFI actions may be beneficial depending on the objectives of the farm and the associated environmental outcomes. However, from a purely economical and time management perspective, it is better to select single or a few actions which provide the greatest return.

If 25% of the farmland was entered into the winter bird food action (option D), there was little benefit to the farm’s net profit level as this option reduced the area for the farm’s cash crops. Carrying out SFI actions at the expense of growing cash crops on productive land had a detrimental effect on the farm’s profitability, at least in the short term, and before any benefits to the productivity of the land materialise.

The additional income the farm receives if it selects actions listed for option B is £28,000–£41,000, as shown in Figure 5.

Figure 5. Three-year projection of income received by 455 ha arable farm from Direct Payments and SFI actions – option B

Source: AHDB

See the breakdown of SFI payments with option B

The income from SFI in year 1 is lower than in years 2 and 3 for some actions, such as IPM2 (flower-rich grass margins, blocks or in-field strips) and AHL1 (pollen and nectar flower mix), because there is an establishment cost in the first year.

In years 2 and 3, the farm receives more income from the SFI actions under option B than it does from direct payments. This highlights the advantage of the more ambitious approach of option B over option A: higher payments are received for more ambitious environmental actions. However, the farm received £104,850 in direct payments in 2020 before reductions began in 2021, highlighting that a considerable gap in income remains.

The 455 ha arable virtual farm in this analysis received between £18,400 and £40,700 in additional income, depending on whether actions under options A or B were undertaken. The more ambitious the actions selected, the higher the extra revenue.

More ambitious actions require additional land; however, if the area where cash crops grow has to be compromised to make space for agri-environmental options, net profit levels are likely to suffer.

If actions can be carried out on unproductive areas of the farm without sacrificing the area of cash crops, an increase in net profit is likely. Such actions may also help regenerate unproductive land and make it more productive in the long term.

The expanded SFI offer gives farmers much more flexibility in terms of choosing actions which suit their farms, but only careful planning and selection will ensure each farmer benefits economically in their particular situation.

No single action in the SFI is going to be enough to mitigate the loss of Direct Payments, but the right combination of actions could go a long way to make up some of the shortfall. This will be more pronounced and helpful to farm businesses in years of average or low crop prices rather than in years in which prices are high. Similarly, farm businesses with lower gross profit levels will benefit more from the SFI than businesses with higher gross profit levels. The SFI will have a role in stabilising farm incomes, as has been the case for Direct Payments and the wider Basic Payment Scheme. Gains from the SFI will be amplified in low/average cost years and for businesses with low gross profit levels. But, if a loss is made, that too will be amplified under these conditions. This highlights the importance of choosing actions with care and making the best-informed plan for your farm.

Sustainable Farming Incentive (SFI)

Environmental Land Management Schemes

Characteristics of top performing farms 2024

Farmbench: A farm business comparison tool